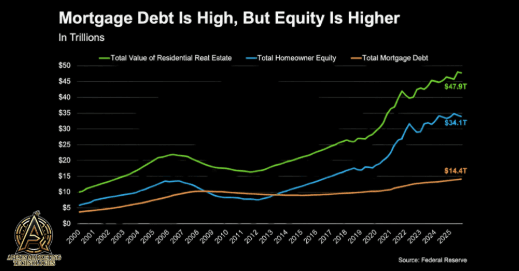

And look, the number itself isn’t fake news. Total mortgage debt in America is currently sitting at a staggering $14.4 trillion.

But while the headlines aren't lying, they are leaving out the second half of the equation. And that second half changes the entire narrative.

To understand why a record-high debt number isn't a sign of an impending crash, you have to look at the full balance sheet of American homeowners.

According to data from the Federal Reserve tracking the housing market from 2000 to today, here is how the numbers actually stack up right now:

Total U.S. Home Values: $47.9 trillion

Total Homeowner Equity: $34.1 trillion

Total Mortgage Debt: $14.4 trillion

Yes, debt is high. But homeowner equity is more than double that debt number, hovering near record highs of its own.

To see why this matters, we only have to look back at the 2008 financial crisis. Between 2008 and 2013, total mortgage debt actually exceeded total homeowner equity. Homeowners had zero cushion. When property values dropped, millions owed more than their homes were worth, leading to widespread foreclosures.

Today, the reality is the exact opposite. The gap between what people own (equity) and what they owe (debt) has never been wider.

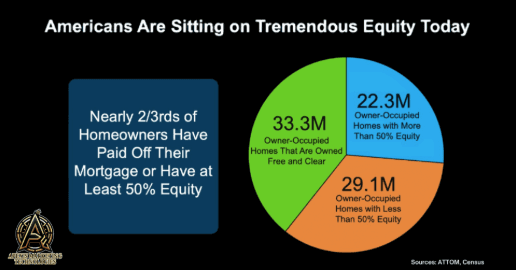

National averages are great, but what does this look like for the average household? Data from ATTOM and the U.S. Census Bureau breaks down the nation's owner-occupied homes into three distinct groups:

Paid Off Completely: 33.3 million homes are owned free and clear. No mortgage, no lender, zero foreclosure risk.

Highly Leveraged Equity: 22.3 million homeowners have more than 50% equity in their properties.

Building Equity: 29.1 million homeowners have less than 50% equity (a perfectly normal status for recent buyers or those paying down newer loans).

When you combine the first two groups, nearly two-thirds of all American homeowners are sitting on massive financial cushions. This isn't a fragile market teetering on the edge of a cliff; it's a market built on an incredibly solid foundation.

Big numbers make for great clickbait, but context is everything.

While mortgage debt is at an all-time high, so is the financial strength of the people holding that debt. The systemic vulnerabilities that triggered the 2008 crash simply are not present in today's housing market.

Wondering what this means for you? Whether you are looking to buy, sell, or just want to know how much equity you've built up in your own home, let’s chat. Reach out anytime to a Apex Mortgage Group Loan Officer for a clear, no-pressure look at your local market.