Chief Executive Officer | NMLS: 176551

While the Department of Veterans Affairs (VA) home loan benefit has been around for over eight decades, deep-seated myths still prevent service members from utilizing it. Let's dismantle the four biggest misconceptions holding Veterans back so you can claim the benefits you've rightfully earned.

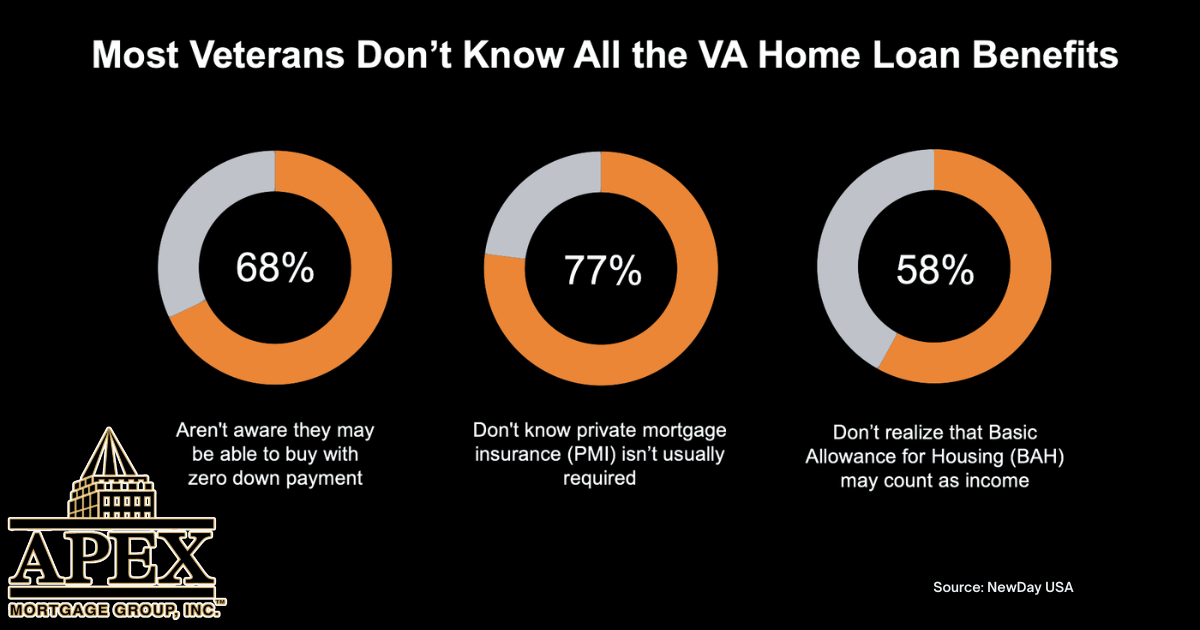

The absolute biggest hurdle for most prospective homebuyers is scraping together a massive down payment. Interestingly, the NewDay USA survey found that many Veterans assumed they needed to save between $10,000 and $19,900 before buying.

The Reality: One of the most powerful features of a VA loan is the ability to buy a home with $0 down. Skipping years of aggressive saving means you could transition from renting to owning much faster than the average civilian.

Beyond the down payment, "closing costs" (the fees required to finalize a mortgage) often catch buyers off guard. Fortunately, the VA has strict regulations that limit the types of closing fees a Veteran can be charged. By keeping more cash in your pocket on closing day, the VA loan program significantly lowers the upfront financial barrier to entry.

With traditional mortgages, if you put down less than 20%, lenders force you to pay Private Mortgage Insurance (PMI). This protective fee typically tacks an extra $100 to $300 per month onto a mortgage payment.

Conventional Loans: Require PMI until you build up 20% equity.

VA Loans: Require $0 in monthly PMI, even with zero money down.

Over the lifespan of your loan, eliminating PMI saves you thousands of dollars and keeps your monthly payment highly affordable.

If you are currently on active duty or serving as a qualifying reservist, your income math looks a little different—and lenders know it. Your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) can be counted as qualified income when applying for a VA loan.

Because both BAH and BAS are non-taxable, they carry extra weight during the underwriting process. If you haven't been factoring these allowances into your homebuying budget, you likely qualify for a higher loan amount than you think.

The VA home loan program was designed to reward your service by turning the dream of homeownership into a tangible reality. The perceived barriers of massive down payments, hidden fees, and expensive monthly insurance simply don't apply to you in the same way they do to others.

If you are a Veteran, an active-duty service member, or a military family member, don't let myths delay your future. Connect with a trusted, VA-approved lender like Apex Mortgage Group today to evaluate your benefits. You might just find out that your timeline to buy a home is right now.

Chief Executive Officer

Apex Mortgage Group, Inc | NMLS: 176551